It's not clear whether Republicans have given up on caring about the economy or if their ideology blinds them to what even sharp high school students can see. What I do know is that a horde of friends who - presumably fed by Fox news or other conservative news outlets - were loudly fretting about deficits during the recovery are now mum about the deficits that will follow from Trump's new tax cut.

One of the simplest things we know about economies is that when unemployment is high you should increase the size of deficits and when unemployment is low you should lower the size of deficits. This is so obvious that it hardly merits mention and yet Republicans seem to miss this point. I don't know if it is because of a paradigm filter, crass disregard for the larger economy, or simple opportunism that comes from disregarding any goals but tax cuts.

Deficits stimulate the economy. That said, there are deficits that are good stimulants and deficits that are poor. The best deficit comes from spending money on things like infrastructure that will leave an economy more able to grow. Ideally, a deficit stimulates the economy short term and lays the foundation for higher productivity in the future. The worst deficit just adds more money to wealthy people who are unlikely to spend much of it. (If your net worth is $3 million and you get another $10,000 in tax cuts, you are less likely to spend any of that money than someone whose net worth is $10,000.) Good or bad, a deficit stimulates the economy, although to different degrees.

As trade makes up a bigger part of the economy, deficit spending it more likely to drive up asset prices like stocks and homes; rather than see a rise in the price of apples, you might see a rise in the price of Apple stock.

(Yes there are other factors. No I'm not going to cover those here.)

Why does this matter? Well, you can't just say that it is good or bad to increase the size of a deficit. If you suffer from high unemployment, increasing deficits is great; if you are enjoying low unemployment, increasing deficits is bad. Atop that, deficits that build the economy's capacity (borrowing to invest in building freeways or high speed rails or basic research or education initiatives) are better than deficits that just create a temporary blip in spending (e.g., tax cuts).

The year before George W. Bush took office, unemployment averaged 4%, its lowest since 1969. It seems safe to say that the economy was at full employment. What did George W. Bush do once he took office? He cut taxes to stimulate the economy. What happened? The price of homes - assets - and the mortgage back securities that financed their purchase went up. Spectacularly. This stimulus created a bubble and bubbles burst. The year before Bush took office unemployment averaged 4% and the year after he was in office it averaged 9.3%. Stimulating an already strong economy turned out to be disastrous.

The first year of Trump's presidency, unemployment will average 4.4%, its lowest since Clinton's last year in office. What does Trump do? He is cutting taxes to stimulate the economy. This could feed a bubble in asset prices ... a bubble that will pop more spectacularly than it otherwise would have. Stimulating a weak economy can create a strong one; stimulating a strong economy can create a bubble.

The Republicans who hollered about deficits during the Great Recession are now creating a deficit in a time of full employment.

It seems as though Republicans like deficits in good times and hate them in bad times.

The question is, why? This is not a difficult concept to grasp and yet Republicans refuse it.

I can only think of a few reasons.

One, they want tax cuts more than they want a healthy economy. They really do think it's possible to live like the rich in banana republics, comfortable even when the larger economy is bad, and as long as they get their tax cuts they don't really care about the larger economy.

Two, they don't believe that macroeconomic policy makes any difference, instead believing that individuals make all the difference. (It is true that individuals make a difference; some do well in bad economies and some do badly in good economies. It is not true that recessions hit because the percentage of lazy people in an economy suddenly doubles, because of changes in individual behavior. The strategies to get near the top of a group are different from the strategies to move a group's median income up.)

Three, they can't distinguish between individuals and a community when it comes to who should get a loan. It is true that you don't want to loan to a guy who is out of work and you'd be happy to loan to a guy with a great job. In that sense they are right that deficits are "safer" when the economy is good. But of course debt is very different for an economy than it is for an individual or household. Even a household engages in deficit spending when times are bad and pays down debt when times are good; if you are unemployed you borrow from your savings or friends; if you are fully employed you save. The banker may rather loan to the guy with a job but it is the guy who is temporarily out of work who most needs the loan. It may seem safe to create more debt in the economy when times are good but that stimulates spending that threatens to create bubbles.

What will be the result of the Trump tax cut? The economy will get worse. Not immediately. Immediately it will get better because the start of bubbles are the best part; it's the busting of bubbles that is miserable.

R World (Ron Davison muses aloud)

Showing posts with label tax cuts. Show all posts

Showing posts with label tax cuts. Show all posts

02 December 2017

Why the Republican Tax Cuts Won't Help the Economy: Understanding the Difference Between the Economies and Parties of Lincoln and Trump

Trillions in excess reserves, cash and negative interest rate bonds calls into question Republican's claim that the economy needs tax cuts to create additional capital.

Abraham Lincoln was the first Republican president. He was part of a visionary party who realized that the industrial economy had changed the rules in a few ways. One, it made capital even more important than land. Two, it made slavery, which was always immoral, now bad economics. Three, it made the national economy most relevant to good policy (goods now produced in growing factories were now transported across state lines by growing railroads to be sold in department stores all across the country) rather than the old state economy. When the south seceded, the largely Republican northern legislators passed a flurry of laws to accommodate this new industrial economy that was supplanting the agricultural economy.

Since the time of Lincoln, a key to understanding Republican policy and strategy is understanding that they believe that nothing is more important to economic prosperity than capital.

There is good reason for such a belief. If you are working with your bare hands you do well to create more than a few pennies - maybe a few dollars - of value a day. If you have capital equipment like a vehicle, a lathe, a computer or factory, you can potentially create thousands - even millions - of dollars in value each day.

The thinking behind the Republican tax breaks traces back to this belief that they need to encourage more investment by corporations by taxing them less. Their belief is that as more money is invested in things like lathes, computers and factories, American workers will be more productive. As it has since the time of Lincoln, more capital from more investments will make us more prosperous.

It is true that capital is essential to our economy. So is agriculture. There is a difference, though, between knowing that we'd perish without farmers and expecting agriculture to employ a growing number of people. In 1800 about 90% of Americans worked in agriculture; by 2017, about 1 or 2% do. Agriculture is essential but that is very different from saying that more farmers will make our country more prosperous. Agriculture is not the place we look in 2017 for the creation of new jobs and wealth.

Capital, too, is essential but that is different from saying that more capital will make us more prosperous. Manufacturing (admittedly just one manifestation of capital) is not the place we look in 2017 for the creation of new jobs and wealth. As farming before it, jobs in manufacturing have been in steady decline as a percentage of the workforce since about 1940.

Again, the simple justification for Republican tax cuts is the belief that they will result in more capital investment. The story of excess reserves calls that into question.

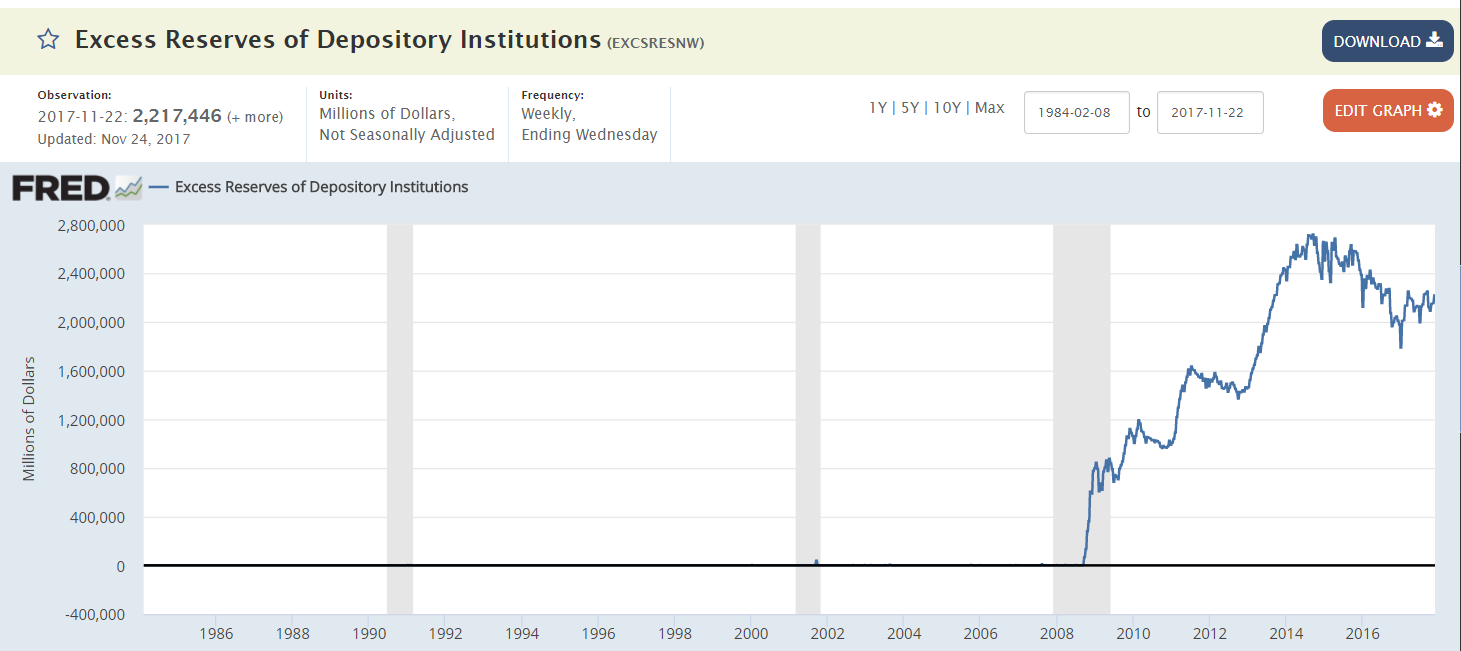

From the early 1980s through 2008, excess reserves in the US banking system mostly bounced around between $1 and $2 billion dollars. Banks are required to keep a certain level of reserves on hand, essentially money they hold in case you come in to make a withdrawal on your account. And simply because it is nearly impossible to have every dime "working" as loans, etc., banks also keep a little reserves in excess of what is required. They have an incentive to keep these reserves to a minimum because they just sit there idle, generating no interest, so it makes sense that they wouldn't hold much in excess reserves.

Then we got hit with the Great Recession. One huge risk was that the credit system would collapse. Among other things, the Fed pumped capital into the banking system to encourage economic activity. The Fed could put capital into the banking system but banks had to put it out into the economy via loans to households and businesses.

Banks are literally professionals at understanding credit risk and knowing when to loan money for a kitchen remodel or a business expansion. Bankers - like business executives, teachers, police, and engineers - make mistakes but this matter of deciding where capital should be employed to maximize the returns on capital is quite literally their job. If they have a billion dollars, they will look for a way to invest or loan that out in order to create a return. Only as a last resort will they leave it idle and not making money.

So what happened when the Fed pumped a record amount of money into the banking system? You can see that below; the one to two BILLION became two to three TRILLION, a jump of 1,000X.

Janet Yellen has helped to engineer a draw down of these excess reserves without disrupting the economy but after peaking at $2.7 TRILLION in 2014, excess reserves are still $2.2 trillion.

Bankers - the experts on capital allocation - are letting trillions sit idle because they don't see profitable ways to employ this capital. Another way to put it is that they don't see capital as scarce.

Excess reserves are not the only bits of evidence that the economy has an abundance of capital. Last year companies in the S&P 500 spent $536.4 billion on buybacks. What does that mean? They spent half a trillion simply buying their own stock rather than investing that money into hiring, factory expansion, or advertising. Like bankers, big corporations don't see capital as scarce but instead see it as abundant, literally having more than they can use. Corporate cash is close to $2 trillion.

The Dutch have financial records that go back 500 years. Think about all that has transpired since 1517: the Protestant Revolution and religious wars that killed tens of percent of the population in certain regions of Europe, coming to an understanding that Columbus had actually discovered new continents and then settling those Americas, democratic revolutions, the industrial revolution, world wars, a Great Depression .... these 500 years have hardly been uneventful. And yet, last year was the first time that the Dutch recorded the sale of negative interest rate bonds. You give a country $100 and get back $99. The Netherlands, the EU, France, Japan .... nine countries had issued about $12 trillion in negative interest rate bonds as of last year

To sum up, US banks have $2.2 trillion in reserves, the S&P 500 has $2 trillion in cash (even while spending half a trillion a year on buybacks), and there are more than $12 trillion in negative interest rate bonds around the world.

None of this suggests that the West faces a scarcity of capital.

So let's get back to the Republican tax cut. The thinking behind it is simple: if we tax less there will be more capital and that capital can be employed to expand businesses that will generate more profit and jobs. And that, of course, assumes that capital is scarce.

Capital was scarce 150 years ago during Lincoln's presidency. At that time, nearly any policies that encouraged the growth of capital were likely to have a positive effect on the economy, helping to make us all more prosperous.

Capital is now abundant. Policies that starve public education and research to send back more capital to corporations and individuals will hurt economic growth, not help it. There is no way that someone can look at the evidence and conclude that what our economy lacks now is capital. There is no way, of course, unless you have failed to update what was once a great perspective to adjust to a new landscape. The party of Lincoln has given way to the party of Trump and mindful intelligence that carefully considers new facts has given way to mindless ideology that ignores them.

Abraham Lincoln was the first Republican president. He was part of a visionary party who realized that the industrial economy had changed the rules in a few ways. One, it made capital even more important than land. Two, it made slavery, which was always immoral, now bad economics. Three, it made the national economy most relevant to good policy (goods now produced in growing factories were now transported across state lines by growing railroads to be sold in department stores all across the country) rather than the old state economy. When the south seceded, the largely Republican northern legislators passed a flurry of laws to accommodate this new industrial economy that was supplanting the agricultural economy.

Since the time of Lincoln, a key to understanding Republican policy and strategy is understanding that they believe that nothing is more important to economic prosperity than capital.

There is good reason for such a belief. If you are working with your bare hands you do well to create more than a few pennies - maybe a few dollars - of value a day. If you have capital equipment like a vehicle, a lathe, a computer or factory, you can potentially create thousands - even millions - of dollars in value each day.

The thinking behind the Republican tax breaks traces back to this belief that they need to encourage more investment by corporations by taxing them less. Their belief is that as more money is invested in things like lathes, computers and factories, American workers will be more productive. As it has since the time of Lincoln, more capital from more investments will make us more prosperous.

It is true that capital is essential to our economy. So is agriculture. There is a difference, though, between knowing that we'd perish without farmers and expecting agriculture to employ a growing number of people. In 1800 about 90% of Americans worked in agriculture; by 2017, about 1 or 2% do. Agriculture is essential but that is very different from saying that more farmers will make our country more prosperous. Agriculture is not the place we look in 2017 for the creation of new jobs and wealth.

Capital, too, is essential but that is different from saying that more capital will make us more prosperous. Manufacturing (admittedly just one manifestation of capital) is not the place we look in 2017 for the creation of new jobs and wealth. As farming before it, jobs in manufacturing have been in steady decline as a percentage of the workforce since about 1940.

Again, the simple justification for Republican tax cuts is the belief that they will result in more capital investment. The story of excess reserves calls that into question.

From the early 1980s through 2008, excess reserves in the US banking system mostly bounced around between $1 and $2 billion dollars. Banks are required to keep a certain level of reserves on hand, essentially money they hold in case you come in to make a withdrawal on your account. And simply because it is nearly impossible to have every dime "working" as loans, etc., banks also keep a little reserves in excess of what is required. They have an incentive to keep these reserves to a minimum because they just sit there idle, generating no interest, so it makes sense that they wouldn't hold much in excess reserves.

Then we got hit with the Great Recession. One huge risk was that the credit system would collapse. Among other things, the Fed pumped capital into the banking system to encourage economic activity. The Fed could put capital into the banking system but banks had to put it out into the economy via loans to households and businesses.

Banks are literally professionals at understanding credit risk and knowing when to loan money for a kitchen remodel or a business expansion. Bankers - like business executives, teachers, police, and engineers - make mistakes but this matter of deciding where capital should be employed to maximize the returns on capital is quite literally their job. If they have a billion dollars, they will look for a way to invest or loan that out in order to create a return. Only as a last resort will they leave it idle and not making money.

So what happened when the Fed pumped a record amount of money into the banking system? You can see that below; the one to two BILLION became two to three TRILLION, a jump of 1,000X.

Janet Yellen has helped to engineer a draw down of these excess reserves without disrupting the economy but after peaking at $2.7 TRILLION in 2014, excess reserves are still $2.2 trillion.

Bankers - the experts on capital allocation - are letting trillions sit idle because they don't see profitable ways to employ this capital. Another way to put it is that they don't see capital as scarce.

Excess reserves are not the only bits of evidence that the economy has an abundance of capital. Last year companies in the S&P 500 spent $536.4 billion on buybacks. What does that mean? They spent half a trillion simply buying their own stock rather than investing that money into hiring, factory expansion, or advertising. Like bankers, big corporations don't see capital as scarce but instead see it as abundant, literally having more than they can use. Corporate cash is close to $2 trillion.

The Dutch have financial records that go back 500 years. Think about all that has transpired since 1517: the Protestant Revolution and religious wars that killed tens of percent of the population in certain regions of Europe, coming to an understanding that Columbus had actually discovered new continents and then settling those Americas, democratic revolutions, the industrial revolution, world wars, a Great Depression .... these 500 years have hardly been uneventful. And yet, last year was the first time that the Dutch recorded the sale of negative interest rate bonds. You give a country $100 and get back $99. The Netherlands, the EU, France, Japan .... nine countries had issued about $12 trillion in negative interest rate bonds as of last year

To sum up, US banks have $2.2 trillion in reserves, the S&P 500 has $2 trillion in cash (even while spending half a trillion a year on buybacks), and there are more than $12 trillion in negative interest rate bonds around the world.

None of this suggests that the West faces a scarcity of capital.

So let's get back to the Republican tax cut. The thinking behind it is simple: if we tax less there will be more capital and that capital can be employed to expand businesses that will generate more profit and jobs. And that, of course, assumes that capital is scarce.

Capital was scarce 150 years ago during Lincoln's presidency. At that time, nearly any policies that encouraged the growth of capital were likely to have a positive effect on the economy, helping to make us all more prosperous.

Capital is now abundant. Policies that starve public education and research to send back more capital to corporations and individuals will hurt economic growth, not help it. There is no way that someone can look at the evidence and conclude that what our economy lacks now is capital. There is no way, of course, unless you have failed to update what was once a great perspective to adjust to a new landscape. The party of Lincoln has given way to the party of Trump and mindful intelligence that carefully considers new facts has given way to mindless ideology that ignores them.

12 October 2017

Unemployment Rate: What is Next After the Longest Drop in History?

We have data on monthly unemployment rates in the US from January 1948 - shortly after World War 2 - through September of 2017. During that time it has never been lower than 2.5% (which it was in May and June of 1953 at the peak of the post war recovery) and never been higher than 10.8% (which it was in November and December of 1982 in the depth of the Volcker-induced recession during Reagan's first term).

Half the time it is below 5.7% and half the time it is above 5.7%.

Unemployment rates of 3.8% or lower put you in the top 10%; rates of 7.9% or higher put you in the bottom 10%. 80% of the time, unemployment rates have bounced between 3.9% to 7.8%; that range defines normal. Outside of that range things are great or awful.

At the depth of the Great Recession - in October of 2009 - unemployment hit 10%. That's among the worst 1% of all months. (Well, in the worst 1.2%.) Since then it has steadily come down during the longest uninterrupted streak of job creation on record. Last month - the end of the streak - unemployment hit 4.2%, a value in the best 17%. We're in the top 20% but not yet top 10%, really good but still not great.

One simple answer as to whether unemployment will drop further is to say that it's only been lower than its current rate of 4.2% 15% of the time. Again, unemployment rates bounce between 4% to 8% most of the time; it doesn't seem to last long outside of that range. That alone suggests that the unemployment rate will soon stabilize or even rise.

Another interesting thing to note is that this is an exceptionally long recovery. Unemployment peaked 8 years ago this month - in October of 2009. A steady drop in unemployment has never lasted longer. The next longest improvement, the drop from the 10.8% high in December of 1982 to its low of 5% in March of 1989, took just over 6 years before beginning to rise again. Unemployment rates steadily drop for a time and then steadily rise, and steady improvements usually last just a few years, not 8 yerars.

At the start of a recovery people are well aware of all the reasons things can go badly. After all, they are just coming out of a period in which things did, indeed, go badly. Remember how early in the recovery people were anxious about Greece, China's stock market, deficit spending, the mortgage market, Greece, etc. People were looking for reasons that things could go wrong. Now? Now they're looking for reasons that the recovery could continue and less aware of reasons it might not; this makes economies more vulnerable.

There are reasons the unemployment rate could drop further and reasons it won't.

Among the reasons it could drop further is that our labor force is growing more slowly than it did a decade ago. From 1955 to 2005, US labor force (folks aged about 25 to 65) grew 1.7 percent a year. Since then it has grown about 0.5%. As companies seek to hire, they'll have fewer options; all else being equal, this would translate into lower unemployment.

Another reason it could drop further is because of a drop in immigration. Again, this lowers the number of available workers and could mean that employers will draw from the unemployed rather than the newly available. If immigration rates drop enough, the labor force might even stop growing.

Curiously, the reasons that the unemployment rate could start to rise again include a drop in immigration. Immigrants don't just find work here. They buy houses, clothes, meals and all the things that drive demand for goods and services that, in turn, drives demand for employees here. If Trump's policies are successful at slowing down the flow of immigrants, he'll actually succeed at destroying jobs.

Trade, of course, could still provide jobs for American workers. Assuming, of course that Trump does not ignite trade wars. Simply put, he wants trade wars with our biggest trading partners - threatening to blow up Nafta and trade deals with China - and if he gets his way we'll see a drop in trade with our three biggest trading partners. That will destroy American jobs.

The third reason that the unemployment rate could rise is because Trump is planning to cut spending and taxes. Tax cuts will disproportionately go to the rich. If you give a poor guy a $1,000 in tax cuts, he's likely to spend $900 of it. When you're making only $30,000 a year, you could use that extra $1,000. If, by contrast, you give a rich guy $1,000 in tax cuts, he's likely to save $900 of it. When you're already making $500,000 a year, an extra $1,000 isn't going to change your vacation plans. Government spending ripples throughout the economy in ways simple (the employees of the State Department buy coffee at that little coffee shop across the street) and complex (the Medicare recipient pays a medical bill which enables the hospital to make a down payment on a new imaging technology and the young doctor to make a down payment on a new car). If you cut $1,000 in government spending and then give a $1,000 tax cut to someone rich, you'll reduce spending, reducing demand for the goods and services that drives demand for employees.

What is the punchline? It depends on whether Trump ends trade deals. In either case, unemployment rates are likely to start rising again within 3 to 9 months. If he ends trade deals, they'll begin to rise sharply.

If Trump fails to end trade deals:

Unemployment will fall to no lower than 3.8% within the next six months, after which time it'll start to rise again. Given drops in the growth of the labor force, job creation could turn negative at least one or two more months within the next year even as the unemployment rate remains relatively stable.

If Trump succeeds in ending trade deals like Nafta:

Unemployment will - at best - hit 4% near term but may have already bottomed out at the current 4.2%. We'll have a recession and the unemployment rate will rise to 6% to 8% within a year or two.

Half the time it is below 5.7% and half the time it is above 5.7%.

Unemployment rates of 3.8% or lower put you in the top 10%; rates of 7.9% or higher put you in the bottom 10%. 80% of the time, unemployment rates have bounced between 3.9% to 7.8%; that range defines normal. Outside of that range things are great or awful.

At the depth of the Great Recession - in October of 2009 - unemployment hit 10%. That's among the worst 1% of all months. (Well, in the worst 1.2%.) Since then it has steadily come down during the longest uninterrupted streak of job creation on record. Last month - the end of the streak - unemployment hit 4.2%, a value in the best 17%. We're in the top 20% but not yet top 10%, really good but still not great.

One simple answer as to whether unemployment will drop further is to say that it's only been lower than its current rate of 4.2% 15% of the time. Again, unemployment rates bounce between 4% to 8% most of the time; it doesn't seem to last long outside of that range. That alone suggests that the unemployment rate will soon stabilize or even rise.

Another interesting thing to note is that this is an exceptionally long recovery. Unemployment peaked 8 years ago this month - in October of 2009. A steady drop in unemployment has never lasted longer. The next longest improvement, the drop from the 10.8% high in December of 1982 to its low of 5% in March of 1989, took just over 6 years before beginning to rise again. Unemployment rates steadily drop for a time and then steadily rise, and steady improvements usually last just a few years, not 8 yerars.

At the start of a recovery people are well aware of all the reasons things can go badly. After all, they are just coming out of a period in which things did, indeed, go badly. Remember how early in the recovery people were anxious about Greece, China's stock market, deficit spending, the mortgage market, Greece, etc. People were looking for reasons that things could go wrong. Now? Now they're looking for reasons that the recovery could continue and less aware of reasons it might not; this makes economies more vulnerable.

There are reasons the unemployment rate could drop further and reasons it won't.

Among the reasons it could drop further is that our labor force is growing more slowly than it did a decade ago. From 1955 to 2005, US labor force (folks aged about 25 to 65) grew 1.7 percent a year. Since then it has grown about 0.5%. As companies seek to hire, they'll have fewer options; all else being equal, this would translate into lower unemployment.

Another reason it could drop further is because of a drop in immigration. Again, this lowers the number of available workers and could mean that employers will draw from the unemployed rather than the newly available. If immigration rates drop enough, the labor force might even stop growing.

Curiously, the reasons that the unemployment rate could start to rise again include a drop in immigration. Immigrants don't just find work here. They buy houses, clothes, meals and all the things that drive demand for goods and services that, in turn, drives demand for employees here. If Trump's policies are successful at slowing down the flow of immigrants, he'll actually succeed at destroying jobs.

Trade, of course, could still provide jobs for American workers. Assuming, of course that Trump does not ignite trade wars. Simply put, he wants trade wars with our biggest trading partners - threatening to blow up Nafta and trade deals with China - and if he gets his way we'll see a drop in trade with our three biggest trading partners. That will destroy American jobs.

The third reason that the unemployment rate could rise is because Trump is planning to cut spending and taxes. Tax cuts will disproportionately go to the rich. If you give a poor guy a $1,000 in tax cuts, he's likely to spend $900 of it. When you're making only $30,000 a year, you could use that extra $1,000. If, by contrast, you give a rich guy $1,000 in tax cuts, he's likely to save $900 of it. When you're already making $500,000 a year, an extra $1,000 isn't going to change your vacation plans. Government spending ripples throughout the economy in ways simple (the employees of the State Department buy coffee at that little coffee shop across the street) and complex (the Medicare recipient pays a medical bill which enables the hospital to make a down payment on a new imaging technology and the young doctor to make a down payment on a new car). If you cut $1,000 in government spending and then give a $1,000 tax cut to someone rich, you'll reduce spending, reducing demand for the goods and services that drives demand for employees.

What is the punchline? It depends on whether Trump ends trade deals. In either case, unemployment rates are likely to start rising again within 3 to 9 months. If he ends trade deals, they'll begin to rise sharply.

If Trump fails to end trade deals:

Unemployment will fall to no lower than 3.8% within the next six months, after which time it'll start to rise again. Given drops in the growth of the labor force, job creation could turn negative at least one or two more months within the next year even as the unemployment rate remains relatively stable.

If Trump succeeds in ending trade deals like Nafta:

Unemployment will - at best - hit 4% near term but may have already bottomed out at the current 4.2%. We'll have a recession and the unemployment rate will rise to 6% to 8% within a year or two.

09 September 2017

Why Kim Jong-un Isn't Giving Up His Nuclear Arms and Trump Isn't Passing Tax Reform

Kim Jong-un of North Korea is not giving up his nuclear arms. The US demanded that Libya's Gaddafi and Iraq's Hussein give up or stop weapon development programs and then later helped their enemies kill them. Kim Jong-un isn't about to trust the US and will keep his nuclear arms in order to keep the US at (nuclear) arms length. If he gives it any thought - and it seems he has - he never give up the nuclear arms that force the US to take him seriously.

Assuming that Donald Trump is as thoughtful as Kim Jong-un, he won't pass tax reform. Why? Once Republicans have that, they will do far less to resist Mueller's investigation even if that investigation leads to impeachment. Right now the GOP doesn't want to risk losing a rare instance in which they have the House, Senate, and Presidency. At least until they get their very important tax cuts.

Assuming that Donald Trump is as thoughtful as Kim Jong-un, he won't pass tax reform. Why? Once Republicans have that, they will do far less to resist Mueller's investigation even if that investigation leads to impeachment. Right now the GOP doesn't want to risk losing a rare instance in which they have the House, Senate, and Presidency. At least until they get their very important tax cuts.

Subscribe to:

Posts (Atom)