A fascinating thing has happened over the last 200+ years of progress, ever since Jefferson changed John Locke's "life, liberty and property" into "life, liberty and the pursuit of happiness."

Since Jefferson life expectancy has doubled and per capita GDP has gone up 25X, the average American now making as much in two weeks as the average American in the late 18th century made in a year.

But the pursuit of happiness doesn't always take individuals into greater prosperity or longer lives.

Some people prefer less stressful, lower-paying jobs or no job at all, choosing less prosperity. Others love hobbies like base jumping or binge drinking, pursuing happiness in a way that also lowers life expectancy. So, while this pursuit of happiness has given most of us more income and longevity, it doesn't have to.

Which brings me to Texas Republicans.

Last week, the Texas GOP voted on their 2022 platform. Quite simply, they refute every advance that has made us more prosperous and longer living than the first Americans.

Jefferson was one of the big reasons we have religious freedom and freedom from religion. His -and all the founding fathers' - Enlightenment philosophy replaced belief in the supernatural with evidence found in the natural. This made science and tinkering rather than personal revelation the stuff of community. It also made things like votes you could count rather than the divine rights of kings the source of power.

The Texas GOP would like to "return Christianity to schools and government," making religion the basis for education and government, a reversal of what Jefferson did centuries ago. They also want to undo the progress of Lincoln.

Lincoln not only fought the Confederacy but instituted income tax. Income tax was a brilliant innovation that gave the Union money to fight Confederates while at the same time investing in the largest infrastructure project in history (the transcontinental railroad) and new universities like the University of California, Purdue, LSU, Texas A&M and dozens of other universities. The A&M designation was for agricultural and machinery, these institutions making American farms the most productive in the world and helping to create a new generation of factory workers. Almost as importantly, the income tax paid interest on the bonds that financed all of these investments, and this turned a generation of ordinary people - shopkeepers, farmers, and housewives - into capitalists whose first foray into investments came through the purchase of these bonds. The growth in capital markets after this helped fund a proliferation of new products, jobs and the most remarkable change in prosperity ever witnessed.

Texas Republicans want to eradicate income tax, a tool for so much including public investments and research that has furthered progress. While tearing down income tax, though, they do want to preserve monuments to the Confederate soldiers who violently resisted Lincoln’s efforts to liberate and improve the lives of all Americans.

Texas Republicans also want to return us to the economic policies of the Great Depression.

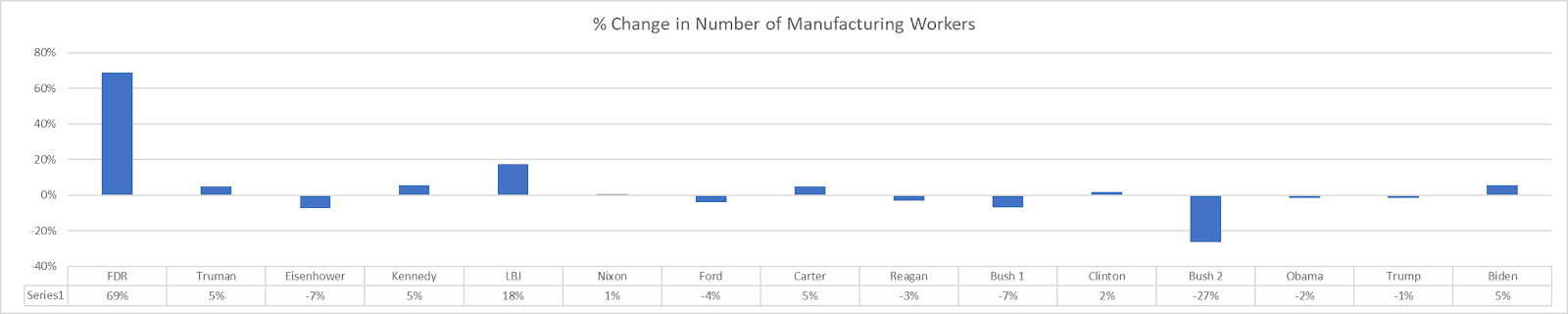

FDR became president in the midst of a brutal economic downturn. The Great Depression destroyed half of GDP and a quarter of American jobs. The global depression drove a similar downturn in Germany, which brought Hitler to power. FDR used the insights of Keynes to begin a recovery but it wasn’t until war with Hitler that government policies drove enough spending to end the Depression. The Federal Reserve pre-dated FDR but he helped to transform it into a vehicle for Keynesian policies. From 1900 to 1933, the American economy was in recession 47% of the time. Since 1933, it has been in recession only 13% of the time, largely changed by a Fed enabled by Keynesian philosophy.

The Texas GOP wants to end the Fed, to return us to the time of unregulated banking. We know how deregulation works and the problems are not limited to the early 1900s. Starting in 2007, Texan George Bush's deregulation of the mortgage market triggered a sharp downturn, a global recession. Had it not been for that recession triggered by deregulation, the American economy would have been in recession only 4% of the time this century, about one tenth as often as it was in the first decades of the last century. The Fed and regulation makes a difference.

In the 1960s, women, minorities and homosexuals gained more rights, access to universities and workplaces. Women could open checking accounts without their husband's signature and won control over their own bodies. The Texas GOP wants homosexuality treated as an abnormal lifestyle choice and wants to end abortion rights.

The pursuit of happiness has neatly coincided with growing prosperity. For Texan Republicans it is not enough to return to a time 250 years earlier before the great advances of Jefferson, Lincoln and FDR. They want to bring along the rest of the state – even the nation - ending hard fought for rights and policies of America’s most defining leaders.

The Texan GOP wants to reverse the great progress that Jefferson, Lincoln, and FDR gave us, policies that gave us longer, more prosperous lives. We are now in a time in history when a growing portion of conservatives so yearn for the imagined past that they are no longer interested in progress but instead imagine their happiness in the past. That would seem almost quaint if their choice was to retreat to off-the-grid communes rather than insist on dragging their neighbors and the rest of the country with them.